Many organizations are coming under increasing pressure to minimize the environmental impact of their activities, as well as optimizing resource consumption to enhance the company's cash flow. Material flow cost accounting (MFCA) is a tool that can help an organization do so by providing a means to trace waste, material, energy losses, and emissions through its processes and activities.

- Material Flow Cost Accounting: Key Facts at a Glance

- Environmental Costs Are Often Left Out

- Material Flow Cost Accounting (MFCA): Developed in Germany, Popular in Japan

- Quantify Material Losses in Monetary Units and Identify the Greatest Savings

- MFCA in Practice

- Resource Efficiency Reduces Operation Costs

- MFCA: Scalable to Your Needs

- Expand MFCA to the Supply Chain Level

- Standardised Methodology: ISO 14051, ISO 14052, and ISO 14053

- MFCA Gains Traction in Japan and the Asia-Pacific Region

- LCA Software Umberto Includes MFCA Tools

- Make Better, Sustainable Decisions

- Frequently Asked Questions

Material Flow Cost Accounting: Key Facts at a Glance

-

MFCA traces material, energy, and emission flows through production processes and assigns monetary costs to losses — making the true price of waste visible.

-

Costs are divided into four categories: material, energy, system, and waste management costs — each allocated to both products and material losses.

-

The methodology is governed by three ISO standards: ISO 14051:2011 (general framework), ISO 14052:2017 (supply chain implementation), and ISO 14053:2021 (phased implementation for SMEs).

-

MFCA is fully scalable — from a single production process to a complete supply chain — and applicable for organizations of any size.

-

IPOINT's Umberto LCA software supports MFCA implementation alongside LCA, carbon footprinting, and material flow analysis.

Environmental Costs Are Often Left Out

MFCA falls within the set of tools used in environmental management accounting (EMA). EMA methods deliver a means of connecting a company's environmental and economic performance, and provide a financial incentive for organizations to more consciously consider the sustainability aspect of their operations.

These tools were developed in recognition that environmental costs were often left out of conventional management accounting techniques, leading to ill-informed or poor decision-making with both environmental and economic consequences. EMA has provided a way to illustrate how improving environmental performance can also improve a company's bottom line.

Material Flow Cost Accounting (MFCA): Developed in Germany, Popular in Japan

MFCA is one of the key tools within environmental management accounting. Developed in Germany in the late 1990s, it has become most prominent in Japan. The method increases the transparency with which a company can trace the flows, transformations, stocks, and losses of physical inputs — including materials, energy, and emissions — through its processes.

As the common saying goes: "you can't manage what you can't measure." MFCA provides a framework for measuring and better understanding resource usage, so organizations can take meaningful steps to manage waste streams and reduce material losses.

Quantify Material Losses in Monetary Units and Identify the Greatest Savings

Reducing resource consumption provides clear environmental benefits — but the crucial aspect of MFCA is that it quantifies the effect of material losses in monetary units. This gives organizations a direct financial incentive to act, because ultimately it affects the bottom line.

In many cases, standard accounting and management systems fail to include or underestimate the level of associated costs for material losses. In MFCA, once the flow model of material usage has been developed, costs can be assigned to the losses throughout the full value chain. This allows organizations to more effectively understand and target the areas where they can make the greatest savings.

MFCA in Practice

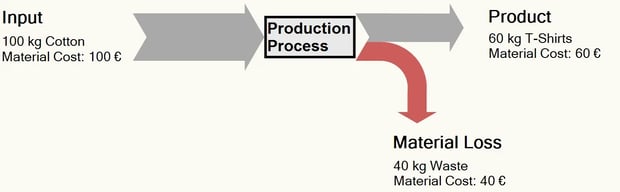

How does this accounting method work in practice? At its core, MFCA applies the principles of mass/material balance. Imagine it in its most basic form: a single process in a t-shirt production line.

A certain amount of textile material is fed into a processing unit (technically termed a "quantity center"), and a certain amount of product — t-shirts — comes out. If 100 kilograms (kg) of cotton go in and 60 kg of t-shirts come out, then 40 kg of material was lost in the manufacturing process. This is what MFCA calls a "material loss." When inputs and products don't balance, material has been "lost" somewhere in the process.

In MFCA models, the flow of resources — materials, energy, water, air, wastewater — is measured in physical units such as mass or volume. The next step is to assign monetary costs to each of these physical flows and losses.

Four types of costs are quantified: material, energy, system, and waste management costs. These are assigned to products and material losses based on the proportion of inputs that flow into each. In the example above, if the cotton input cost €100, the economic material loss equals €40 — since 40% of the material was wasted. Energy and system costs (40% of the processing unit's running costs) and waste management costs for handling the unused cotton must be added as well.

Resource Efficiency Reduces Operation Costs

By conducting this analysis, an organization can not only see where it loses resources — with the resulting environmental impact — but also where it loses out economically in its production processes. This gives companies the incentive to use resource efficiency as a means to reduce operation costs, with the sustainability benefits that come along with it.

MFCA: Scalable to Your Needs

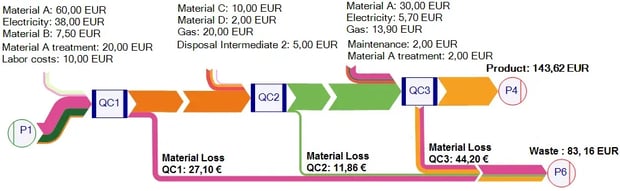

When developing an MFCA flow model, one of the key decisions is defining the system boundary. The tool can be scaled up or down to cover as much or as little as an organization desires: a single isolated process, a whole factory production line, or a product's full supply chain. This scalability means an organization can identify the largest inefficiencies across its activities and most effectively target the areas where it can make the greatest savings.

The figure above depicts a sample case with three quantity centers (QC) including further cost types beyond direct material costs. The accumulated costs associated with each QC sum up to the total waste costs.

MFCA is also increasingly relevant for organizations pursuing circular economy strategies. By identifying where materials are lost — and at what cost — it creates the data foundation for closed-loop thinking: pinpointing where material recovery and reuse would deliver both environmental and financial returns.

Expand MFCA to the Supply Chain Level

Product design generally involves an array of integrated processes and suppliers, each with their own inefficiencies and losses. These losses can have unseen and unconsidered effects on the environmental and economic cost of a final product — no link in the supply chain is isolated from the processes occurring up and downstream.

One of the most significant developments in MFCA has been its extension across a product's full supply chain. From this perspective, MFCA principles can also be applied to enhance Life Cycle Assessment (LCA) tools. Expanding the model boundary to the supply chain level not only gives an individual company a better understanding of its resource and financial losses, but also motivates a larger number of suppliers and firms to evaluate their own inefficiencies.

In this way, MFCA can act as a driver for company collaboration to optimize full-chain resource efficiency.

Standardized Methodology: ISO 14051, ISO 14052, and ISO 14053

To standardize the MFCA methodology, ISO developed a framework of three complementary standards within the broader ISO 14000 family of environmental management accounting standards — the same family that includes the LCA standards ISO 14040 and ISO 14044.

ISO 14051:2011 established the general framework for MFCA, covering common terminology, objectives, principles, and implementation steps. It has been reviewed and confirmed as current as of 2025. ISO 14052:2017 extended the standard with practical guidance for implementing MFCA across a supply chain — directly supporting the upstream and downstream collaboration described above.

The most recent addition, ISO 14053:2021, provides phased implementation guidance specifically designed to help SMEs and other organizations begin their MFCA journey in a focused, step-by-step manner. Together, these three standards offer a complete toolkit for organizations of any size.

MFCA Gains Traction in Japan and the Asia-Pacific Region

Despite being developed in Germany, MFCA has gained its largest traction in the Asia-Pacific region, and most prominently in Japan. The Japanese Ministry of Economy, Trade and Industry (METI) played a central role in driving adoption throughout the 2000s and early 2010s. By 2011, more than 300 Japanese companies were using MFCA across a wide range of applications — including manufacturing, logistics, construction, and recycling (JMCA, 2011).

In nearly all documented cases, MFCA proved to be an effective decision-making tool for delivering resource and cost savings. Since then, adoption has grown well beyond Japan, with organizations across the Asia-Pacific region and internationally increasingly recognizing MFCA as a practical tool for meeting ESG commitments and sustainability reporting requirements.

LCA Software Umberto Includes MFCA Tools

EMA software tools continue to evolve — both simplifying the inputs required to use them and enhancing the usefulness of the outputs. Our LCA Software Umberto supports MFCA implementation alongside LCA, carbon footprinting, and material flow analysis, providing a single platform for comprehensive sustainability assessment.

Getting started with MFCA can involve a significant data collection effort — gathering flow data across processes and assigning costs consistently is rarely trivial. Software tools like Umberto reduce this burden considerably by automating flow modeling and cost allocation, so teams can focus on interpreting results and acting on them.

Make Better, Sustainable Decisions

For individuals and organizations with an interest in sustainability and environmental management, the benefits of cutting material loss and waste seem intuitive. The power of MFCA is that it helps this group make better resource management decisions — but also engages those who are less attuned to the benefits of sustainable practice.

By coupling physical and monetary losses, MFCA software demonstrates how optimizing resource efficiency is also effective in cutting operational costs. In other words, building a more sustainable practice model simply makes good business sense.

References

JMCA, 2011. Material Flow Cost Accounting: MFCA Case Examples 2011

Frequently Asked Questions

What is material flow cost accounting?

Material flow cost accounting (MFCA) is an environmental management accounting tool that traces material flows within production processes, quantifies them in physical and monetary terms, and assigns costs to both products and material losses. Standardized through ISO 14051:2011, it helps organizations simultaneously reduce environmental impact and production costs.

What is a material flow?

A material flow refers to the movement of physical inputs — such as raw materials, water, or energy — through a production process from input to output. In MFCA, these flows are measured in physical units like mass or volume and tracked at each step to identify where losses occur.

What is flow cost accounting?

Flow cost accounting is one of the precursor methods on which MFCA builds. It allocates costs to the flows of materials and energy through a process rather than to products alone, helping organizations see where resources are consumed and where losses accumulate.

What are the 4 types of costs in MFCA?

MFCA categorizes costs into four types: material costs, energy costs, system costs (e.g., labor and equipment), and waste management costs. Each type is allocated to both product output and material losses based on the proportion of inputs that flow into each.

What ISO standard governs MFCA?

MFCA is governed by three complementary ISO standards: ISO 14051:2011 establishes the general framework; ISO 14052:2017 provides guidance for supply chain implementation; and ISO 14053:2021 offers phased implementation guidance for organizations and SMEs. All three fall within the ISO 14000 family of environmental management standards.

How does MFCA differ from conventional cost accounting?

In conventional cost accounting, waste costs are typically absorbed into overall production costs, making inefficiencies difficult to identify. MFCA separates and highlights the costs assigned to material losses, giving managers a transparent view of what waste actually costs the business — and a clear financial case for reducing it.